4/8 – 4/12 Red Rock Update

4/8 – 4/12 Red Rock Update

Building Wealth in the Secular Bull Market to 2036

Stocks peak about every 36 years, most recently in 1929, 1965, and 2000. This 36 year cycle can be traced all the way back to the earliest eras in recorded human history, back to Pythagoras and Plato and the Axial Age around 600BC. After each peak comes a period of decline (punctuated by bear market rallies) that typically lasts 16 years or so. Then, with the excesses of the prior bull period wrung out and investors most depressed, the next 20-year run to the next market top can begin. We're in that Golden Age now – take advantage of it!

Howdy, Bull-Riders:

Is the economy hot or not...and does the Fed care? The answer is that it is stronger than the Fed expected, but they don't directly care. What they care about is inflation and unemployment – those are their two mandates.

Inflation

We got the March Consumer Price Index (CPI) inflation report, which is not the Fed’s preferred measure of inflation. They have repeatedly said that they look at the core Personal Consumption Expenditures Index (PCI) to get to their 2% target. The next PCE announcement comes April 26, before the May 1 Fed meeting. March's CPI increase was driven by elements not included in the PCE.

First, the numbers. Headline year-over-year (YoY) inflation was 3.5%. That was up from 3.2% in February and a tick above the 3.4% expectation. The core YoY number, excluding food and energy, was 3.8%, the same as February but also a tick above the 3.7% consensus. Essentially, the markets panicked Wednesday over inflation topping the consensus estimates by a tenth of a percent. The deflation of core goods intensified, showing a YoY decrease of 0.7%, while the growth rate for core services accelerated, reaching +5.4%.

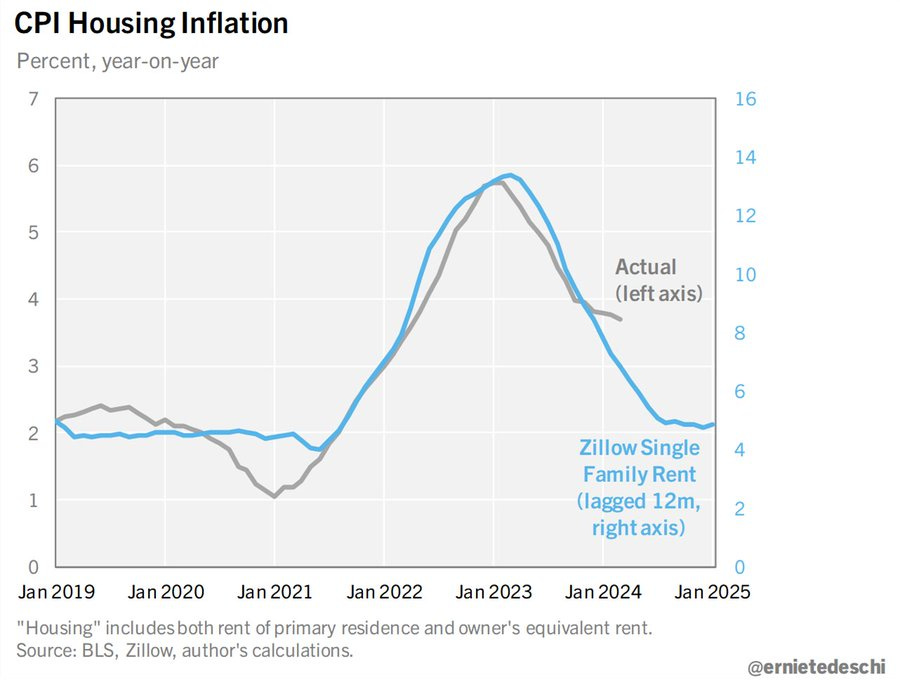

As usual, the lagging Cost of Shelter component contributed most to the slow CPI decline. Cost of Shelter includes the rent paid by tenants for housing and something called Owner Equivalent Rent, calculating the hypothetical amount homeowners would pay to rent their own homes, which obviously is affected by what renters actually pay. The “Rent of Primary Residence” component came in at 5.67% YoY, which was the lowest reading since May 2022, but still reflecting early 2023 rents rather than today's generally lower reality.

@ernietedeschi, former Chief Economist at the White House Council of Economic Advisers, showed how the Zillow single family rent data leads the CPI shelter component by 12 months:

h/t @ernietedeschi

@jayparsons, a rental housing economist, showed this chart:

h/t @jayparsons

Cost of shelter – the two rent measures – accounts for 32% of the CPI and 43% of the core CPI. The blue line above shows real asking rents are up 0.20% YoY, not the 5.68% the Bureau of Labor Statistics used. If we multiply that 5.48 percentage point difference by the 32% that rents account for in the CPI, we get an overstatement of 1.75 percentage points. Subtract that from the 3.5% reported and annual inflation was just 1.75%. Using the same methodology, core CPI falls from 3.8% to 1.5% (h/t @OphirGottlieb).

The month-over-month (MoM) increase was 0.4%, unchanged from February but a tick above economists' forecast. The core MoM increase, which is a marginally useful number for figuring out what is really going on, was up 0.36%, also the same as February and also well above the consensus. A 0.36% monthly increase compounds to well over 4% annual inflation. Not good. The futures market has now pushed out the first rate cut into September. I think that the Fed will either cut by June or not at all to avoid looking partisan in the lead-up to the election. As I've been saying for months, “high – but not higher – for longer.” You heard it here first.

Unemployment

The Bureau of Labor Statistics said the US added 303,000 jobs in March, more than 50% above the consensus forecast for 200,000 and the largest gain in 10 months. The odds of all economists surveyed missing their nonfarm payrolls forecasts by such a wide margin for three straight months seem awfully low to me, but we'll have to wait until after the election to see the final revisions.

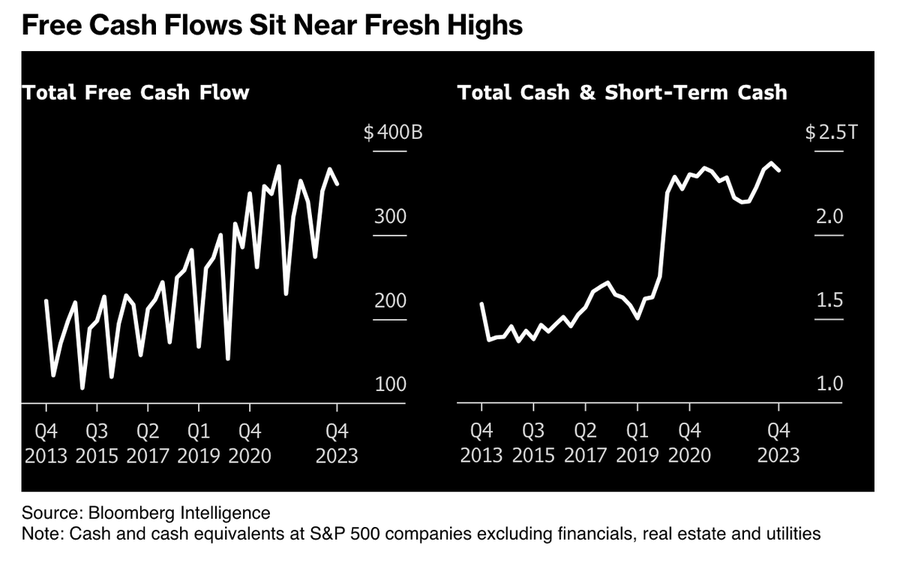

In the real world, corporate cash and free cash flow are at record high levels, supporting stock prices as we head into March quarter earnings results.

h/t @JessicaMenton

Market Outlook

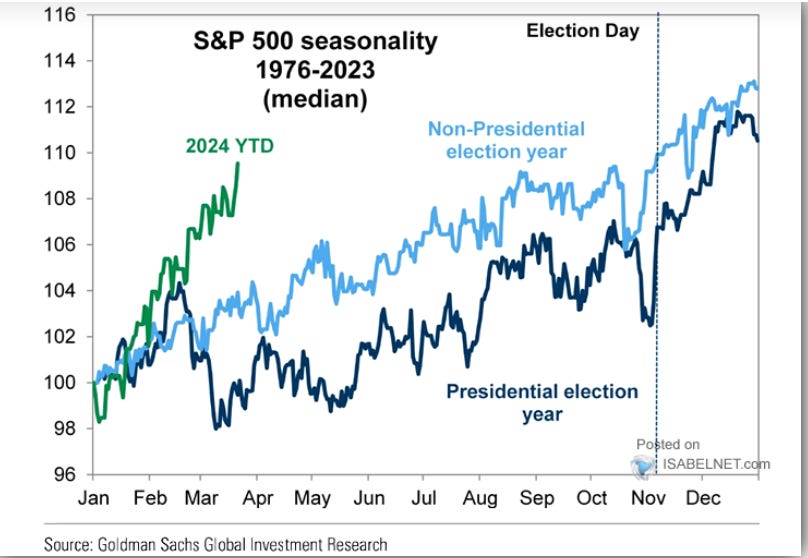

The S&P 500 added 1.0% since last Thursday as inflation reality came in not much worse than – maybe even a little bit better than – inflation fears. The Index is up 9.0% year-to-date, and has been much stronger seasonally that in a typical Presidential election year. You could argue that means (1) it's ahead of itself; or, (2) that it's a powerful sign of underlying strength. I think it's both, so we'll probably see high-level churning through the election.

Although April should get better after next Monday.

The Nasdaq Composite gained 2.4% as investors looked ahead to March quarter earnings, especially in technology. It is up 9.5% for the year. The SPDR S&P Biotech Exchange-Traded Fund (XBI) climbed 2.0% as riskier assets caught a bid. It is only up 2.2% year-to-date, though

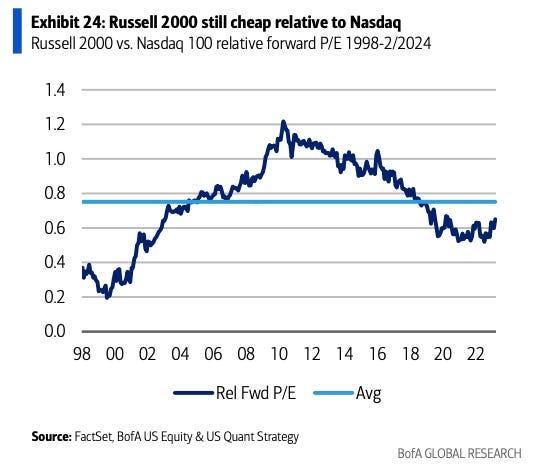

The small-cap Russell 2000 fell 0.5% and is (barely) up 0.8% in 2024. BofA said: “The Russell 2000 remains historically cheap vs. the Nasdaq, and as the overall corporate profits backdrop continues to broaden/accelerate, we see better trends for US small caps.”

h/t @dailychartbook

The newest Conference Board survey showed 49.3% of consumers expect higher stock prices. That number has only ever been higher once, in January 2018 at 51.0%. Following that instance, the S&P had mildly negative returns over the next 12 months, followed by a huge rally.

h/t @dailychartbook

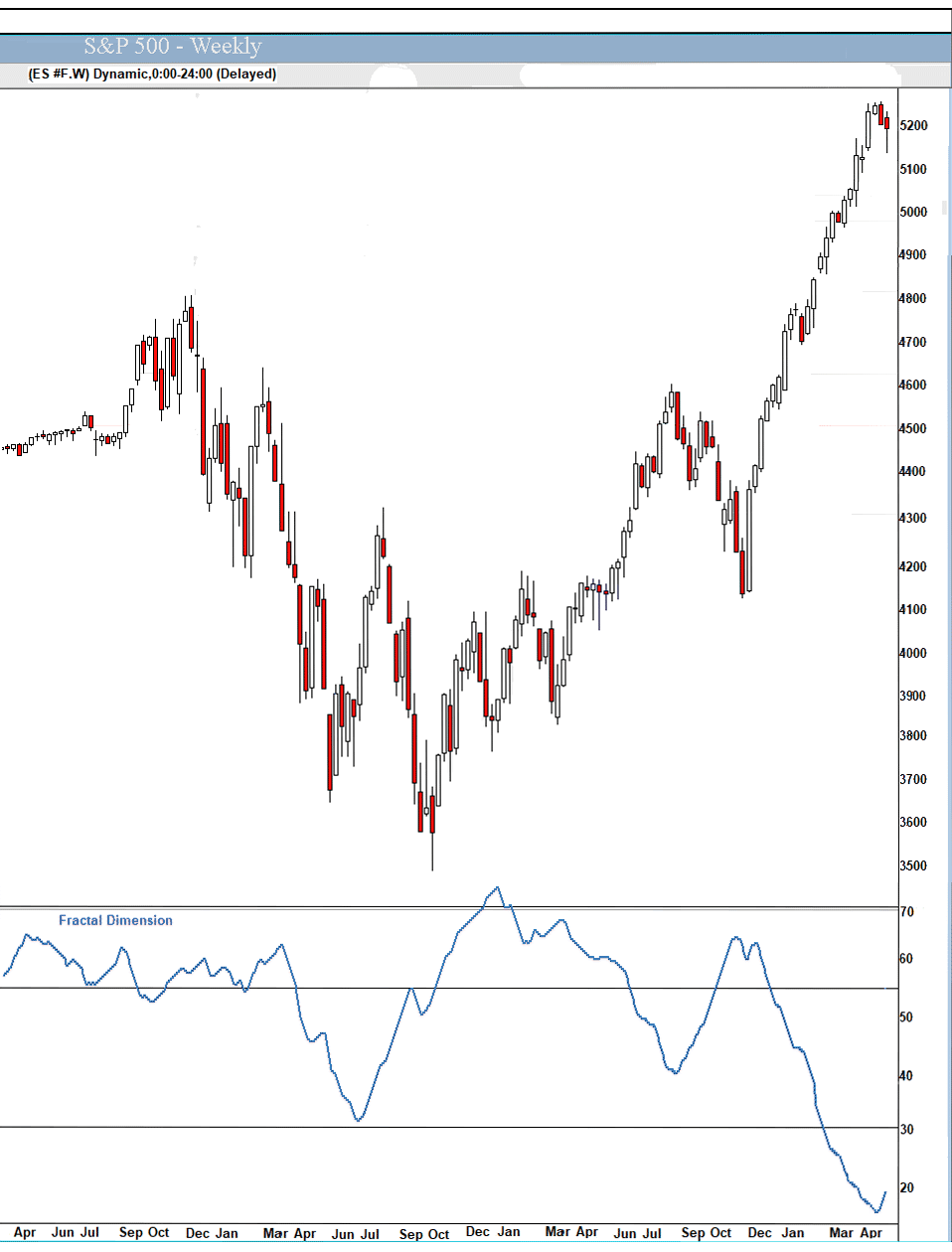

The fractal dimension continues to grind out the necessary consolidation. As I said last week, this could continue for quite a while.

Economy

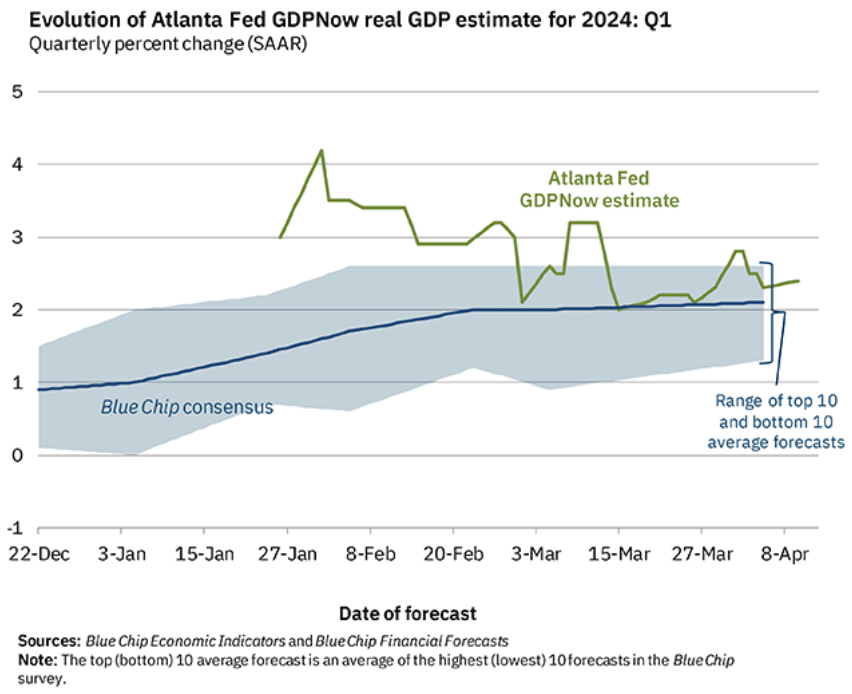

The Atlanta Fed's GDPNow model now is predicting March quarter real GDP growth of +2.4%, still a bit above the consensus for +2.1%. We get the first estimate in two weeks on April 25.

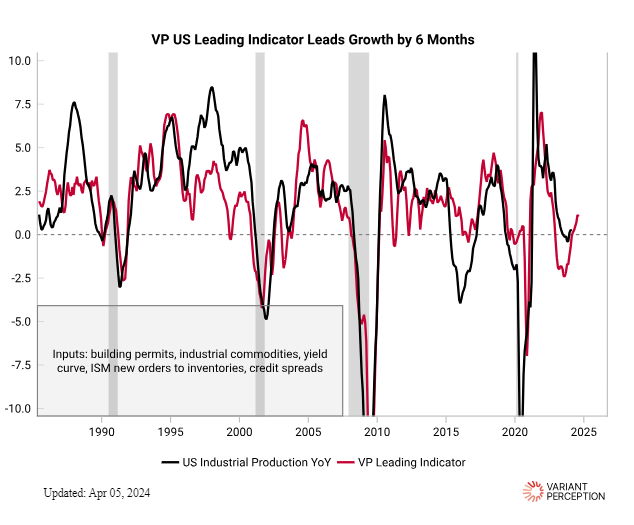

Variant Perception has a proprietary VP Leading Indicator of US economic conditions, and it is clearly inflecting higher:

h/t @VrntPerception

I may have to change my mild recession forecast if this keeps up.

ATTENTION PAID SUBSCRIBERS: Important updates this week on gold, bitcoin, and oil!

Golden Age Portfolio Update

This was a poor week for the portfolio as Wall Street preferred value over growth. It fell 1.6%, but we're still up 19.5% in 2024. Big Tech earnings start to flow in a couple of weeks – that will turn things around with much more to come. Let's dig in...

* * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * *

* * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * *

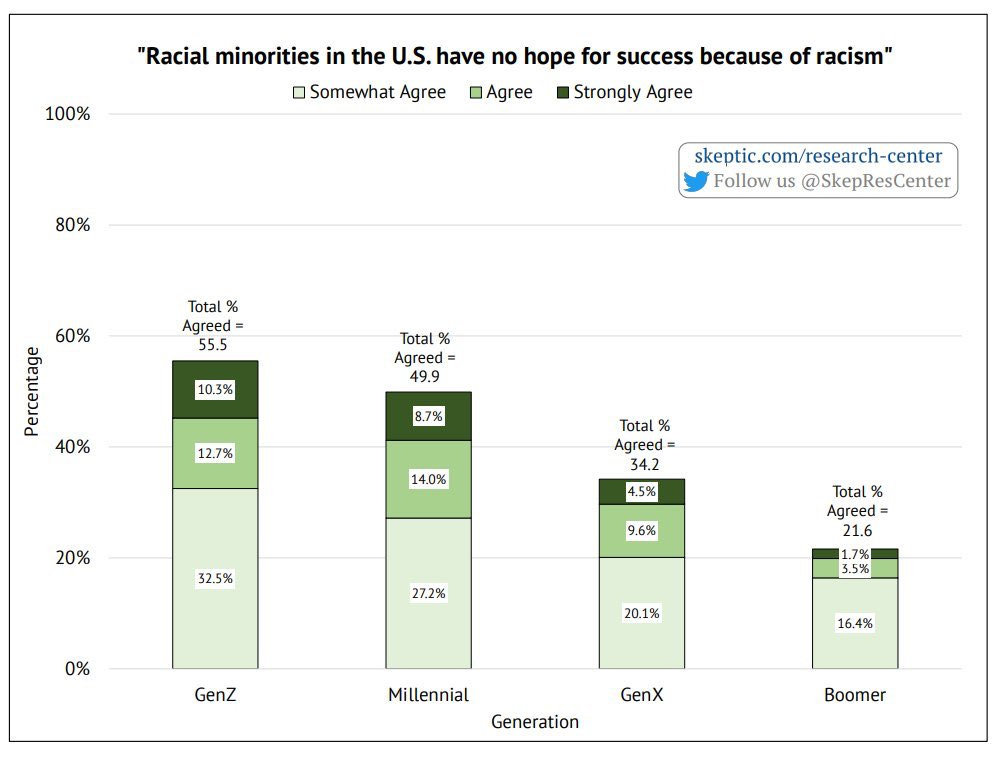

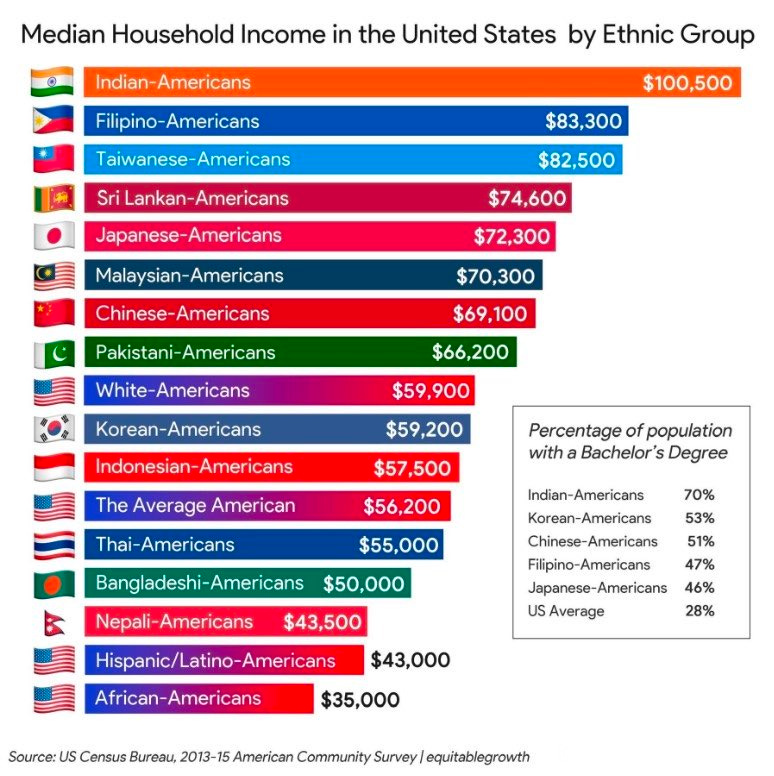

Perception: Almost 50% of Millennials and a majority of Gen Z think “Racial minorities in the U.S. have no hope for success because of racism.”

h/t @TheRabbitHole84

Reality: Some of the most successful groups in the United States are racial minorities.

h/t @TheRabbitHole84

* * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * *

Your reviewing The Battle of the BADS Editor,

Paid subscriber or not, if you would click the ♥ symbol below it would really help me get the word out.