4/15 – 4/19 Red Rock Update

4/15 – 4/19 Red Rock Update

Building Wealth in the Secular Bull Market to 2036

Stocks peak about every 36 years, most recently in 1929, 1965, and 2000. This 36 year cycle can be traced all the way back to the earliest eras in recorded human history, back to Pythagoras and Plato and the Axial Age around 600BC. After each peak comes a period of decline (punctuated by bear market rallies) that typically lasts 16 years or so. Then, with the excesses of the prior bull period wrung out and investors most depressed, the next 20-year run to the next market top can begin. We're in that Golden Age now – take advantage of it!

Howdy, Bull-Riders:

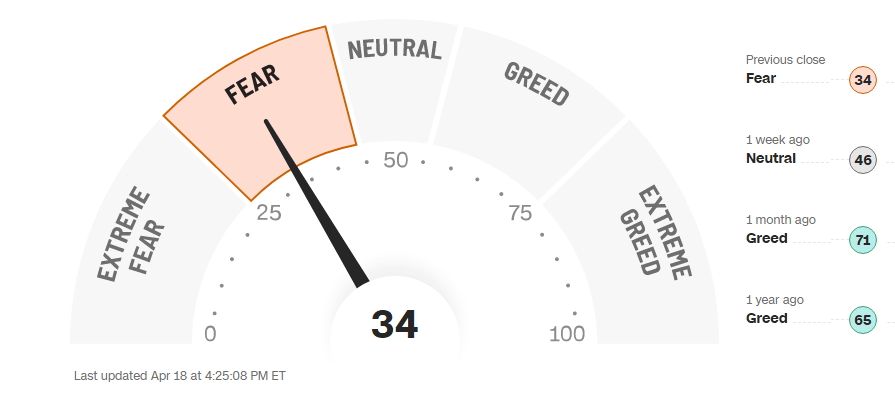

On Tuesday, Fed Chairman Powell said inflation is coming down slower than he expected, so it's “high – but not higher - for longer.” Wall Street did a decent job of panicking the weak hands into selling them some cheap stock as the CNN Fear & Greed Index plunged to its lowest level since November 3.

h/t @WinfieldSmart

But the bond market said: “Whut?” as the 2-year note yield rose a measly two basis points to 4.96% and the 10-yr note yield settled an equally disdainful three basis points higher at 4.66%. Everyone already is on board with the idea that the Fed will lower rates slowly and reluctantly. Wall Street knows a stronger-than-expected economy means stronger-than-expected earnings to support high valuations.

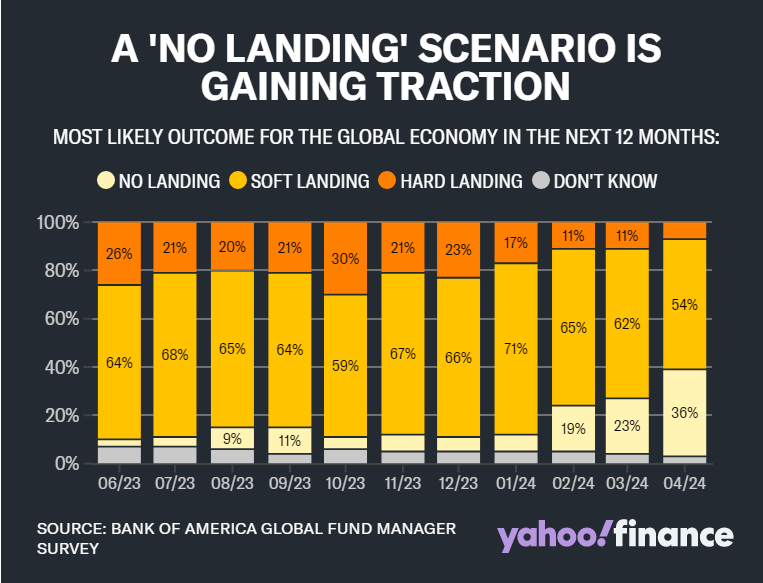

In fact, according to the latest BofA Fund Managers Survey, 36% of fund managers now believe the most likely outcome for the global economy is a "no landing" scenario. This was substantially higher than the 23% who saw the outcome a month ago, and the highest level seen since June 2023.

Jefferies wrote: “Recessions don't hit the US economy without a catalyst of some sort, and we just don't see what is going to stop consumer spending. With demand still solid, it is hard to see how inflation will continue to slow down, and thus it is hard to see how the Fed can cut rates.”

54% of respondents still believe a soft landing - where economic growth slows but not to the point of recession, and inflation returns to its historical average - is the most likely outcome. My scenario – a brief, mild recession that takes inflation below 2% - isn't even a choice.

I am looking at the collapse in the money supply in 2023 plus the employment data showing most new jobs are part-time workers (taking second and third jobs to survive, I suspect) to arrive at my mild recession forecast. If I'm wrong, the “no landing” scenario is the next most likely.

But retail investors still fear the Fed, and net stock buying by corporate insiders of publicly traded companies is the lowest in at least a decade. I think that's just because these are the highest prices they've seen in a decade.

h/t @mayhem4markets

Market Outlook

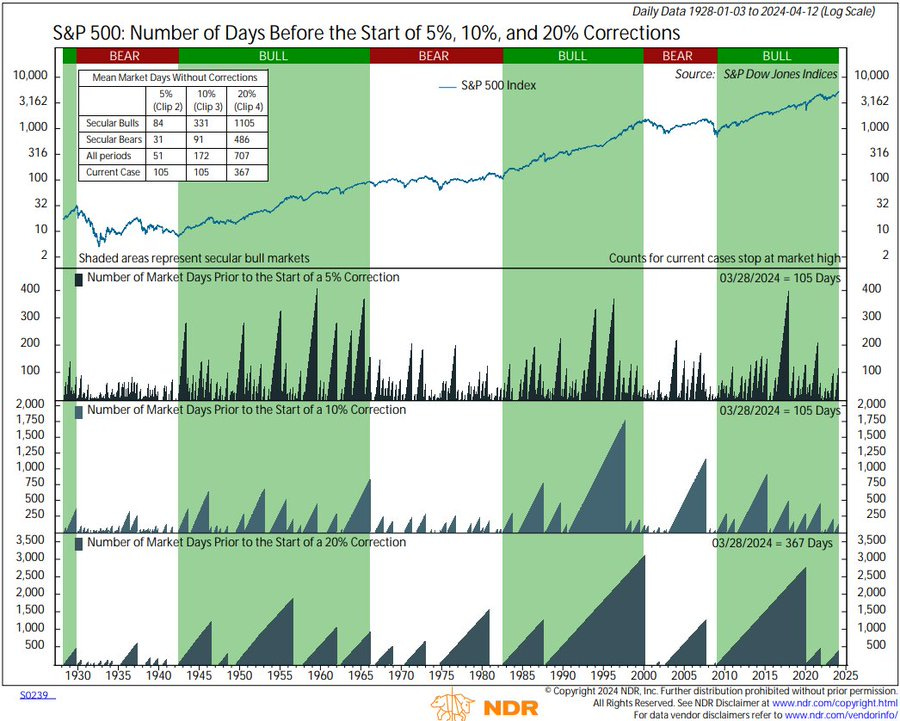

The S&P 500 lost 3.6% since last Thursday as weak hands panicked at “high for longer.” The Index now is only up 5.1% year-to-date. It has been 107 days since the last 5% correction in the S&P. Since 1928, during secular bull markets, 5% corrections occurred about every 84 days on average. It has also been 107 days since a 10% correction. 10% declines typically occurred every 331 days on average during secular bulls. The S&P 500 currently is off 4.82% from its all-time high on March 28 at 5264.85 (h/t @NDR_Research).

h/t @DayHagan_Invest

The Nasdaq Composite lost 5.1% as Big Tech took more hits. It is only up 3.9% for the year. The SPDR S&P Biotech Exchange-Traded Fund (XBI) fell 8.5% as it was clobbered every day this week. It is now down 6.5% year-to-date. The small-cap Russell 2000 dropped 100 points or 4.9%, throwing it back to a 4.2% loss in 2024.

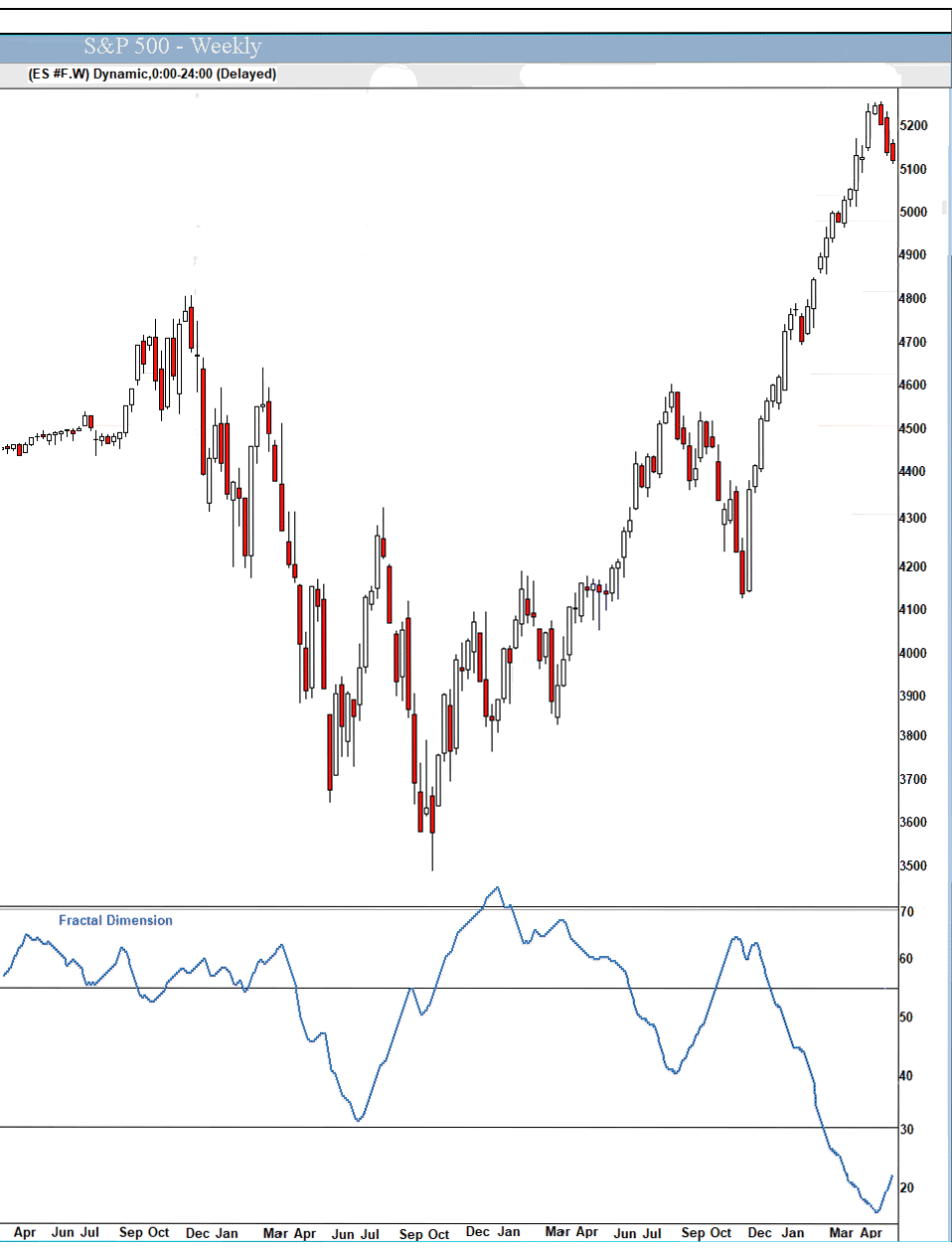

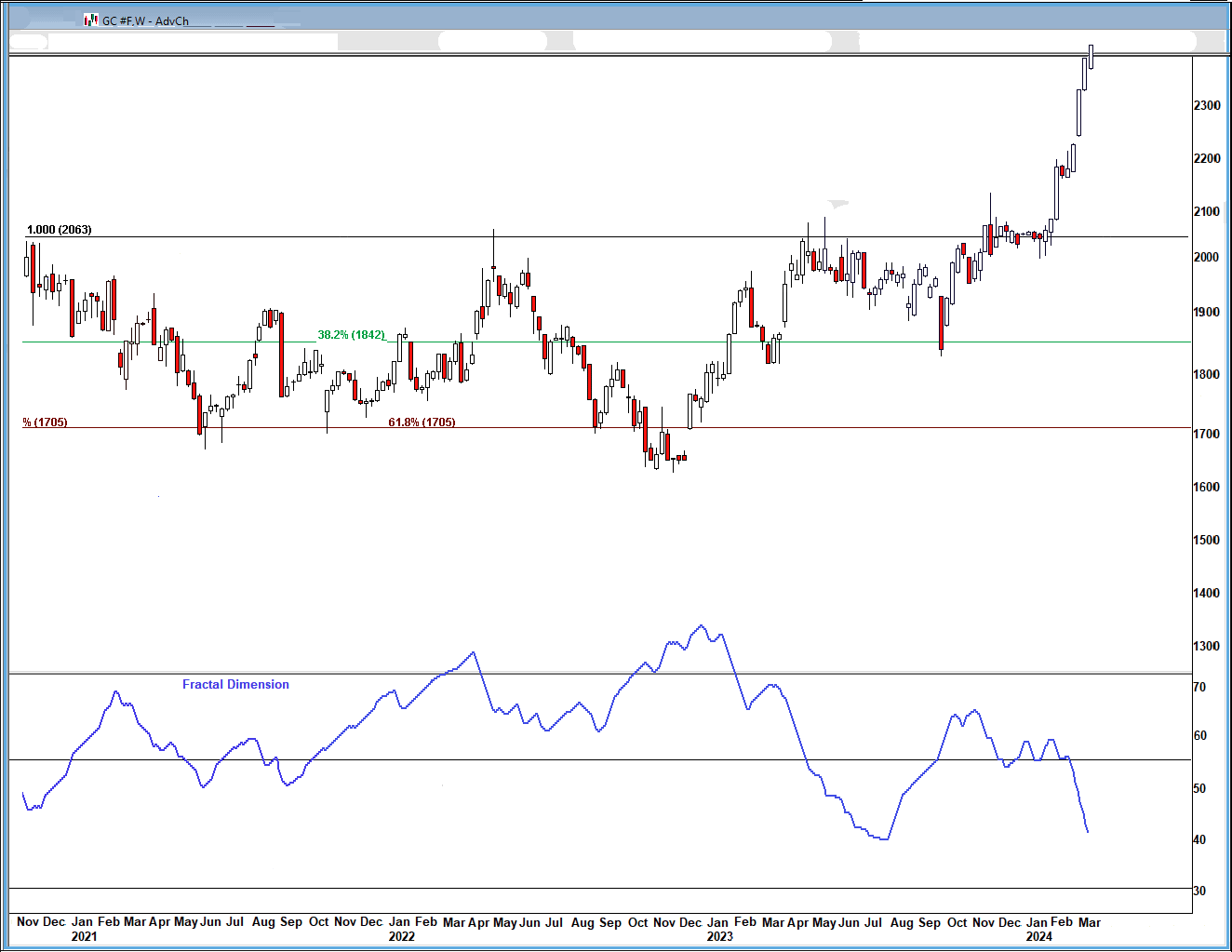

The fractal dimension indicates this correction has either a lot of time or a lot of points to go in order to consolidate the huge upturn from last October. Many recommendations may give us a much better entry point, although not all.

Economy

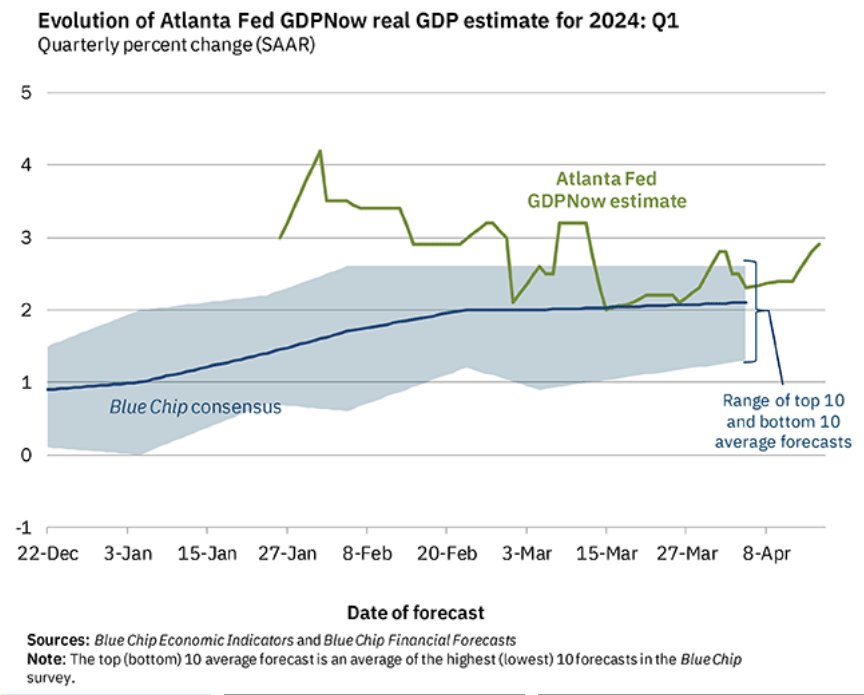

The Atlanta Fed's GDPNow model next-to-last estimate of March quarter real GDP growth ticked up from 2.8% to 2.9% due to a bit of strength in personal consumption expenditures and private domestic investment, The Blue Chip economists are estimating just over 2.0%, so we should see a slightly positive “surprise” on April 25.

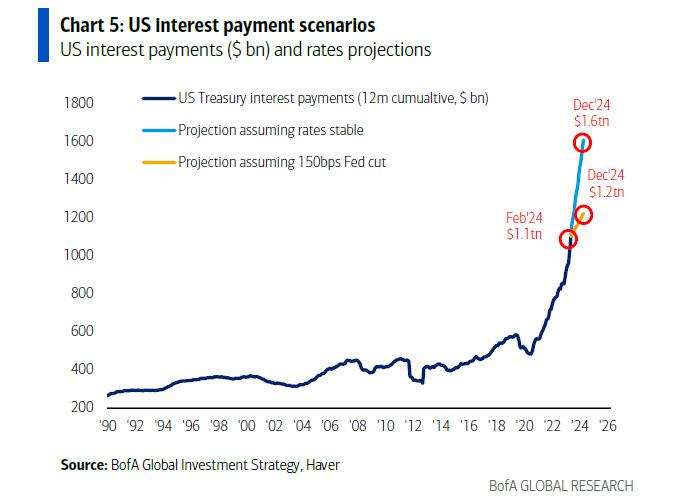

Gold hit new all-time record intraday and closing highs today, over $2,400, even though significant interest rate cuts are off the table as the US possibly approaches the Minsky Moment of issuing $1 trillion in debt every 100 days. Interest on US debt, now at $1.1 trillion, is set to surpass Social Security spending and become the single largest government outlay before the end of the year.

h/t @zerohedge

Gold is up $300 in six weeks, its quickest rise in a decade. In his latest report, BofA CIO Michael Hartnett noted that investors are looking beyond the “here and now,” realizing that there is no way markets or the economy can sustain 5% nominal and 2% real rates, and are hedging two things: (1) the risk that the Fed has to cut as CPI accelerates, and (2, more ominously), the “endgame of Fed Interest Cost Control (ICC), Yield Curve Control (YCC), and renewed Quantitative Easing to backstop US government spending.”

In short, he thinks something big is about to break, and if the surge in gold leads to a spike in yields, start the countdown to one of two things: QE and/or YCC, because if the bond market sniffs out the endgame that gold is currently smelling, it will be up to Powell to once again prevent a catastrophic financial collapse.

BofA commodities strategist Michael Widmer wrote: “Gold and silver are among our most preferred commodities, with the yellow metal pushed up by central banks, China investors and, increasingly, Western buyers on a confluence of macro factors, including an end to hiking cycles. Accordingly, we see the yellow metal rally to $3,000/oz by 2025. Silver benefits from that too, with prices also boosted by stronger industrial demand. This could take prices above $30/oz within the next 12 months.”

UBS wrote: “The recent move in gold reminds me of a famous quote: 'There are decades where nothing happens, and there are weeks where decades happen.' Looking at history, the gold price can stay in the doldrums for a long time, but when it does breakout the surge is usually fast and furious...Should history repeat itself, it is not too late to participate in the current gold rally. An investor with a two- to three-year view could expect to see gold potentially double from here to more than $4,000. The take-profit signal is when real rates turn negative and when there is a full-blown recession. Today with real rates still high and a recession seemingly far away, it is too early to call the end of the ongoing gold rally.”

Costco is making $100 million to $200 million a month selling gold bars, according to a Wells Fargo equity research note. Last October, the company began selling one-ounce bars made of nearly pure 24-karat gold priced at about $2,000. They sell about 2% above spot prices to members before a 2% cash back reward for executive members and an extra 2% in cash back for those with a Citi card.

They also are selling silver coins in tubes of 25. The one-ounce Canada Maple Leaf silver coins were priced at about $680 before selling out online earlier this month. Silver is up more than gold so far this year as 2024 is expected to mark the fourth straight year of a structural deficit, according to the Silver Institute's annual World Silver Survey.

The study showed an estimated global silver market deficit of 184.3 million ounces in 2023, the second-highest deficit on record behind 2022's deficit of 263.5 million ounces. The silver deficit is forecast to rise by 17% to 215.3 million ounces in 2024 due to a 2% growth in demand to a fresh record high of 1.22 billion ounces, led by strong industrial consumption, alongside a 1% decline in total supply.

The fractal dimension continues to signal a trend that can continue for a few weeks before the necessary correction starts.

Coming Events for Free Subscribers

(Additional coming events for paid subscribers below the paywall.)

All times below are ET.

Wednesday, April 24

Short Interest - After the close

Thursday, April 25

March quarter GDP - 8:30am – First estimate

Friday, April 26

Personal Consumption Expenditures Index - 8:30am – The Fed's favorite inflation measure

Golden Age Portfolio Update

This was a very bad week for tech, growth, AI, and the portfolio as it slipped7.4%. We're still up 10.7% in 2024 with much more to come. Some of our recommendations are at extraordinary buy points. Let's dig in...

* * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * *

* * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * *

* * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * *

Your reading The Maintenance Race Editor,

Paid subscriber or not, if you would click the ♥ symbol below it would really help me get the word out.